How Much Should You Bid For Small Businesses?

And Why Valuations Don't Really Matter For Self Funded Search Deals

Buying cheap has been the gospel for investors since the early days of Graham and Buffet. The SMB MBA references a study that found that purchase price was the best predictor for returns and 60% of the returns in private equity deals come from the 25% of companies bought for the lowest multiple. It’s unsurprising that most searchers worry about overpaying and spent excessive amounts of time trying to accurately value potential businesses.

In the next few paragraphs, I will outline why financial performance rather than multiples (aka purchase price) is the key driver of enterprise value for small businesses and how bank requirements and owner alternatives create a relatively tight multiple band (3.0x - 4.5x EBITDA) and therefore searchers should optimize for growth potential and business quality rather than multiple / price.

For large businesses, multiples fluctuate more than financial performance. For small businesses, financial performance fluctuates more than multiples.

Let’s use the simple model where enterprise value is determined by a multiple of EBITDA. In that model, the change in enterprise value is driven by the change in EBITDA (financial performance) and the change in multiples.

Multiples for large companies tend to be much more volatile than the underlying earnings. The volatility is the most pronounced for the largest (public) companies. 50%+ swings in multiples over a 5 year period have happened several times over the last century. While the underlying earnings can also be volatile, investors usually consider adjusted financials when valuing companies (adjusting for one-off bad years).

For small businesses on the other hand. Losing a large customer or having a new competitor can have a significant impact on the financials. However, the multiples are confined to a relatively closed range.

Debt Service Coverage requirements from the banks limit multiples to ~6.0x EBITDA

Self-funded search deals typically maximize SBA 7a financing which leads to a common deal structure with 75% SBA debt, 15% seller note and 10% equity. Debt Service Coverage requirements vary by lender, but usually fall into the 1.2x - 1.5x range.

Assuming the normal 10 year SBA loan with a 6% interest rate and 10% interest on the seller note with no amortization results in a maximum multiple of ~6x EBITDA that would still comply with the Debt Service Coverage.

Since SBA 7a loans are capped at $5mm, this deal structures is limited to businesses with <$1.5mm EBITDA. While 6x EBITDA is too high of a multiple for the vast majority of businesses in this size range, the Debt Service Coverage gives us limit on the upper end.

The bank appraisal further limits the maximum multiple to ~4.5x EBITDA

In order to close the SBA loan, banks require a third party appraisal of the business to support the purchase price. Appraisers use multiples from other transactions of similar size in the same industry.

While there can be exemptions depending on the industry and appraiser, for businesses with less than $1.5mm EBITDA, it is unlikely that the appraisal will support a multiple of 5.0x EBITDA or higher. Therefore, the highest supportable multiple is likely around 4.5x EBITDA.

The business cash flow makes offers below 3.0x EBITDA unattractive to the seller

The limiting factor on the lower end of the valuation range is the owner’s option to simply keep the business and continue to receive the cash flow. Instead of accepting a 2.0x EBITDA offer, the owner could just run the business for 2 more years and receive similar proceeds.

Excluding special situations like large one-off contracts, unique personal challenges, or <$300k EBITDA businesses, offers below 3.0x EBITDA are simply not worth the trouble of going through a sales process for most sellers.

Unlike the multiples for large companies, this multiples band won’t change materially unless the SBA program changes.1

Financial performance becomes more predictable the larger the company

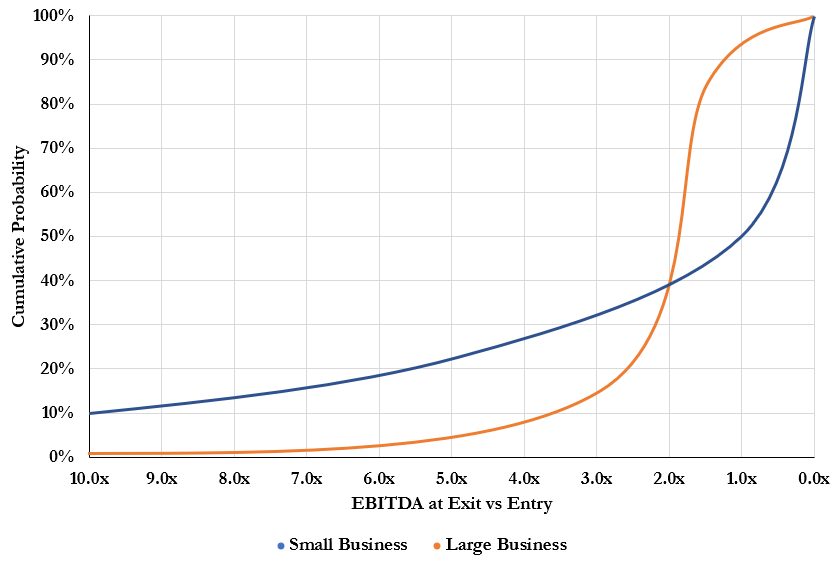

As companies get larger, outsized growth/decline becomes less and less likely. While a local HVAC company can relatively easily double in size over a year, it would be impossible for Walmart to do the same. As a consequence, the larger a company is at acquisition, the more likely it will grow at close to GDP growth. Conversely, 50% of small businesses fail within 5 years, while the remaining 50% are are likely significantly larger than they were 5 years ago.

Overall, the probability distributions looks something like the chart below. Large businesses have a fairly narrow range of financial performance (with EBITDA at exit in the same order of magnitude as EBITDA at entry), while small businesses are more likely to grow significantly or go bankrupt than stay the same size.

Multiples matter for large businesses, growth potential for small businesses

The relatively low volatility of financial performance and high volatility of multiples for large companies explains why buying cheap is paramount. Even good growth in EBITDA for a company this size can be wiped out by a decline in multiples.

For small businesses on the other hand, finding a company that has a good chance of growing EBITDA is a much larger determinant of success than paying a low price since the volatility of financial performance is high, but the multiples are relatively fixed.

Why you should pay up for good businesses

At this point, you might say that paying 4.5x instead of 3.0x EBITDA still means paying a 50% higher purchase price. However, while the math is right, I think there is a better way of thinking about it2.

First, most searchers have limited time to search (usually 1-2 years). Paying up not only increases the odds of getting a deal done, but more importantly greatly increases the odds of getting a deal done early. Paying 4.5x EBITDA at the start of your search is effectively the same as paying 3.5x EBITDA 12 months into the search as the cash generated from the business has already returned ~1.0x EBITDA3. Losing a good business trying to save 0.5x EBITDA on the purchase price is a great way to end the search empty handed.

On the other hand, the wide range of outcomes for small businesses over a 5 year period makes the entry point (with the 3.0x - 4.5x range) almost irrelevant. Even in a scenario where you buy for 4.5x and sell for 3.0x, if you can double EBITDA you still sell for 33% more than you paid. Given multiples increase with the size of the business, it’s unlikely you will sell for a lower multiple than what you bought for if the business has grown.

Rising rates will lower the multiples compliant with the bank’s Debt Service Requirements. However, since currently the appraisal is really driving the upper end, rates will have to raise significantly before Debt Service Requirements are limiting the upper end.

Overpaying is a much bigger issue for larger companies trading in mid- to high teens multiples. Overpaying by 50% on a 15x EBITDA business means 7.5 years of operating cash flow to recoup the overpayments compared to 1.5 years for a 3.0x EBITDA business.

In reality it is likely closer to 3.9x after taxes and fees, but the concept still holds.

Just wanted to say this is an amazing article -- very influential on my thinking