Understanding Search Funds as an Asset Class

How to target the right investors

While the number of search funds has grown rapidly over the past 10 years, search funds as an asset class remain a niche appearance. When looking for investors, it is helpful to understand where search funds sit on the spectrum of asset classes.

Search funds as an asset class fall between growth equity and private equity

Broadly speaking, search funds are part of the private equity asset class. This part is fairly self explanatory, since you are investing in the equity of a private company.

Private equity is historically categorized by the life cycle stage of the company:: venture capital for early-stage, growth equity for mid-stage and private equity for mature companies.

The vast majority of companies acquired by search funds fall into the mature category (established product or service proven over years / decades). However, after considering the deal structure, the risk-return characteristics of self-funded search deals for investors actually look a lot more like growth equity. Just to make sure we are comparing apples to apples, here are the definitions of each term for the purpose of this posts:

Growth Equity: Investments in mid-stage, high growth, profitable companies with a proven product

Self-Funded Search: Acquisition of a small business using SBA 7a loans, searcher pays for the cost of the search

Traditional Search: Acquisition of a small business using conventional debt, searcher raises a fund to pay for search costs

Independent Sponsor: Acquisition of small-to-medium sized business, typically seasoned operators / private equity investors, independent sponsor pays for search costs

Private Equity: Acquisition of medium-sized or large businesses, fund has committed capital and charges management fees to cover search / management costs.

Typical key characteristics for a deal in each asset class look something like this:

Self-funded search is more similar to growth equity, traditional search is more similar to private equity

The reason self-funded search is most similar to growth equity is the risk-return profile and the minority stake character. In growth equity, the risk is driven by the high entry multiple (>20x EBITDA). Since the exit multiple will be significantly lower, the business needs to grow very fast to compensate. For self-funded search the risk is driven by high leverage, which results in material bankruptcy risk. However, in both cases, there is also large upside driven by high growth potential due to the novel product (growth equity) or the small company size (self-funded search).

Traditional search is more similar to the independent sponsor model and traditional private equity. Investors acquire the majority of the company, have material control via the board of directors and the risk-return profile also looks similar (normal leverage levels with modest entry multiples). Traditional search has historically outperformed private equity, driven by the smaller company size and lower entry multiples. On the flip side, traditional search investors give up equity from the start while private equity only participates in the profits (carried interest).

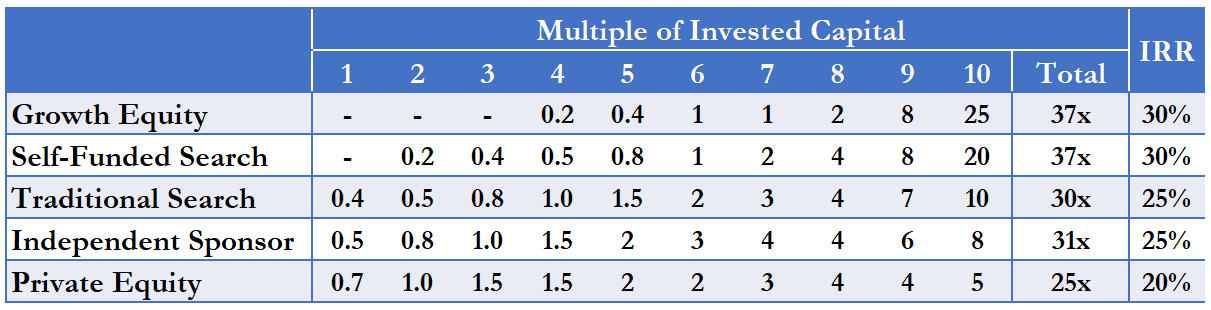

Another helpful angle to understand the similarities and contrasts of the different investments is to look at a successful fund and where the returns come from. The table below assumes a 5 year hold period with 10 investments of equal size and shows an illustrative outcome for each. A multiple of invested capital of 1 means the investors got their money back.

In growth equity and self-funded search, large winners drive the returns of the fund. This is unsurprising, given these two investment types have a significantly wider range of outcomes due to the earlier stage product (growth equity) and high leverage (self-funded search).

For traditional search through private equity, investors are less likely to lose money on a given deal due to the lower risk, but are also less likely to hit a home run.

When raising equity, look for investors that are familiar with similar deal types, not necessarily business types.

In my experience, minority investors and majority investors tend to have fairly different investment philosophies. Minority investors are more focused on the home run, understanding that means striking out a bunch. Majority investors are more focused on finding good companies with incremental improvement opportunities. The lower upside means you can’t afford to lose as often and therefor want tighter control.

Despite coming from a private equity background and having a much broader network there, we raised the majority of our money from the minority investor crowd (start-up types, former self-funded searchers etc.). The idea of only receiving a 20-40% stake in the company despite funding most of the equity felt intuitively wrong to the private equity guys despite intellectually understanding the deal math and that they would receive appropriate upside. For the growth equity / start-up types on the other hand, the deal and structure felt intuitively right, even though we are buying a mature business.

Finally, real estate investors are another large universe that has matching deals to the operating business side. Real estate investors that are involved in higher risk deals (development, rehabs, etc.) could be another good pool of potential investors for self-funded searchers.