What Search Model Is Right For You?

Self Funded vs. Traditional

TLDR: If you can stomach the risk of the personal guarantee, the self-funded model offers more upside, speed and flexibility than the traditional model.

My guess is that most people first find out about the traditional search fund model when they initially come across the search fund concept. The traditional search model has been around for almost 40 years and is more represented in main stream books and publications. The growing community around self-funded search on platforms like Twitter and Searchfunder is a more recent phenomenon and you are unlikely to come across them unless you already know what you are looking for.

Once you made your way into the search fund world, deciding which search fund model to pursue becomes the first major decision.

Historically, searchers had to pick between either going the traditional route or going completely alone. Today, searchers have a spectrum of options depending on four major factors: upside & risk, resources & support, search preferences, and accessibility.

Self-funded search models:

Searcher pays the cost of the search including broken deal fees (lawyers, diligence providers, etc. for deals that don’t close)

No committed capital, funds are raised once the searcher has a deal under LOI

Self-funded searchers usually use SBA financing and keep 60-80% of the equity

“No investors”: The searchers has the cash equity to buy the business

“Investors”: More common version, where searcher raises money from investors once they have a deal

“Incubators”: Incubators like Sam Rosati’s Pursuant Search Partners or Tim Ludwig’s Majority Search provide support for the search and transaction in return for fees / investment rights at predetermined terms

Traditional search models:

Searcher raises money from investors to fund a 2 year search. Investors receive the option to invest at predetermined terms

While the capital is not committed, it is more certain than self funded

Traditional searchers usually use conventional bank financing and keep 15-30% of the equity

“Traditional”: Raise money from multiple search fund investors. Investors don’t play an active role in the search

“Accelerators”: Fund pays for the search and provides knowledge and systems for the search process. Most support, most expensive.

Upside and Risk

The upside of owning a successful business is certainly one of the main appeals of starting a search. There are plenty of great articles running through the math of self funded vs traditional searches. However, in order to fully understand the upside for different search models, you have to understand both the returns in different scenarios along with the probability of each scenario.

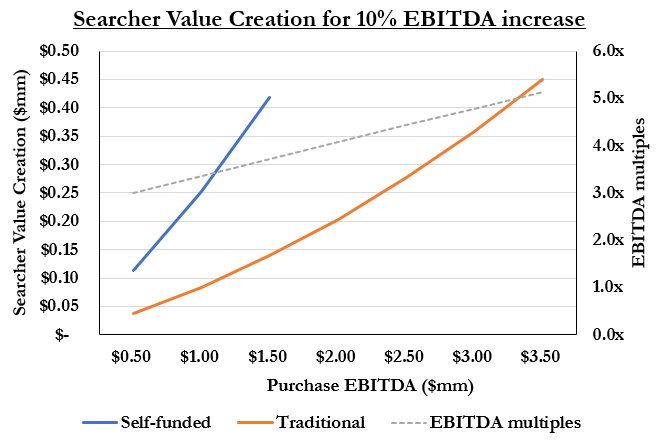

The chart below shows the equity value creation for a searcher for a 10% increase in EBITDA assuming the searcher keeps 75% of the equity in a self-funded search and 25% of the equity in a traditional search. With the SBA 7a program capping out at $5mm, it’s difficult to acquire companies above $1.5mm EBITDA (assuming only 10% equity injection), which is why the self-funded line ends there. Traditional search funds are only limited by investor capital.

Since self-funded searchers keep roughly 3x as much equity as traditional searchers, traditional searchers need to acquire business that are 3x as large to have the same upside.

That leaves a “grey area” for companies between ~$1.5mm - $3.0mm of EBITDA where a searcher could have more upside by buying a significantly smaller business. Once the company size exceeds $3.5mm EBITDA, the upside for traditional searchers is higher than any self-funded search.

Understanding the upside for different company sizes for the two models raises the question of likelihood of finding such a company. Most of the data in that regard is anecdotal evidence (case studies of folks who bought a company of a certain size through the traditional or self-funded model). Since I couldn’t find any good data of the number of companies by size range, I came up with my own estimate. You can read the full process in my post: “What Are Your Odds Of Finding A Company?”

My best estimate is that the pool of available companies for self-funded searchers is at least 5x larger than the pool of available companies with equivalent upside for traditional searchers.

Of course the increased upside comes with significantly higher risk. The SBA 7a loan requires a personal guarantee which means business failures result in personal bankruptcy. Conventional loans used by traditional searchers typically do not require personal guarantees.

The 10 year default rate for SBA 7a loans is somewhere between 15-25%. Self-funded search deals are likely on the lower end compared to the average given they are larger deals (more stable businesses) and usually in less cyclical industries (not a lot of retail / restaurant), but it’s tough to know. The downside of the personal guarantee really depends on the searcher's level of risk appetite / aversion.

Resources and Support

Running a self-funded search requires significant personal resources. Most banks and investors require at least some investment from the searcher (say $50k). Even without an office and living frugally living expenses won’t be much below $50k. Deal transaction cost (lawyers, accountants, bank fees) are likely close to $50k as well (transaction costs are rolled into the deal if successful). Adding it all up, starting with $150k means you essentially get 1 year of runway, one major broken deal and then you have to find your deal. While broken deals can happen, they usually happen earlier in the process, so a broken deal is likely closer to $10k-20k. For a 2 year search, $150k-$200k of starting capital is probably a good number.

Conversely, traditional searchers get paid a salary during their search and can use the funds they raised for an office and transaction costs. Additionally, traditional searchers are not required to invest any of their own money into the deal. Once a traditional search fund is raised, it does not require any capital from the searcher to run a 2 year search and buy a business.

During the search, self-funded searchers are mostly on their own. However, platforms like Searchfunder and Twitter offer answers to almost all questions a searcher could come across and access to other searchers that are going through the process. Solo searches can be a lonely affair and the comradery of the platforms helps. Search fund incubators can also help with aspects like sourcing, business evaluations and deal structuring.

For traditional search funds, the investors can be a valuable sounding board. Most are seasoned search fund investors that have seen numerous funds come and go and can give advice on best practices. The accelerator model takes that approach to the next level by offering searchers a blueprint with all the tools and templates to run their search.

Search Preferences

One of the downsides of the traditional search model is that it typically limits the flexibility of the searcher when it comes to location and industry. With ~80% of traditional search deals coming from proprietary sources and a smaller pool of companies that are large enough, it typically requires searchers to cast a wide net.

Traditional searchers usually can’t limit their search to a certain state, much less a particular city. You might be allowed to focus on a region, if you are flexible regarding the industry. If you are focused on one industry, the search likely has to be nationwide.

Self-funded searchers on the other hand can decide their search parameters independently. If you will only search in a particular city, self-funded is the only option. In that case it’s a good idea to be open to several industries, so the pool of targets does not get too small. Location restrictions often come into play when the searcher has a spouse or family. Would they move to a small town in a state neither of you have been to for the next 5-10 years?

One benefit of a regionally focused search is the additional credibility it gives you with sellers and brokers. Having a similar area code, knowing street names and rooting for the same sports team helps building trust. On the flip side, you might have to source proprietary deals, because there are limited companies listed in any given city.

The last major factor is timing / patience. Self-funded searchers have much higher odds of finding a deal quickly, because they can use brokered deals. In talking to search fund veterans, the consensus was that 80% of self-funded deals are brokered and 80% of traditional deals are proprietary. Due to the company size that traditional searchers are looking for, they compete with private equity and strategics, resulting in low chances of success in brokered deals.

There are good reasons for this dynamic. There is a larger volume of companies in the smaller self-funded range, so searchers can focus on the companies that have the highest likelihood of being sold - the ones listed for sale. Since other buyers in that size range often look similar to searchers with limited involvement of better buyers like private equity and strategics, searchers have realistic chances of getting their offer accepted.

Traditional searchers on the other hand have fairly bad chances in brokered processes. The size of the company they are looking for attracts private equity and strategics that can both pay more and provide higher certainty of close. That’s why traditional searchers are forced to find companies directly through proprietary outreach.

Brokered deals allow self-funded searchers a significantly higher number of at-bats, since the work of gathering the necessary information to assess a company has been done by a broker. For traditional searchers it’s difficult to look at more than a few deals simultaneously since they have to play the information gathering role of the broker in each of them.

Additionally, proprietary deals simply take longer from the time the searcher gets involved until close. My guess is that the information gathering and sales process education take 3-6 months. This is time the searcher can save in a brokered deal.

All in all, it is pretty unlikely to close a proprietary deal in the first year (3 months of fund set up and outreach, 6 months of information gathering and sales process education, 3 months to close). For brokered deals on the other hand, you have 9 months to find a deal and could still close in the first year.

Nick Haschka has written extensively about the benefits of finding something smaller quickly, gaining experience and industry credibility, and then leveraging that position into additional acquisitions.

Accessibility

Even after almost 40 years in existence, the search fund model still remains a niche concept that people usually hear about in their MBA classes at schools like Stanford, Harvard, Wharton, Booth or Kellogg. The current traditional search fund investor universe largely consists of networks tied to those schools that are either former searchers themselves or were successful investing in the space. A few large outliers like Asurion created generational wealth for the investors who since have continued to invest in the space.

Without going to those schools it can be difficult to access theses networks and regular investors are often unfamiliar with the concept. However, top MBA programs have notoriously low acceptance rates. As a result, most prospective searchers won’t have the option to go the traditional route. As a side note, even getting in does not guarantee you will be successful in raising a search fund.

While accelerators don’t have ties to specific schools, the limited spots for each cohort (typically 5-6) create their own barrier of pursuing a traditional search.

The self-funded path on the other hand is open to anyone, as long as you have the savings for 1-2 years of searching.

Conclusion

Over the past few years, the search model has become more and more flexible and the next generation of searchers can customize more than ever. In the current environment with abundant capital, good operators are the value creators and that dynamic is causing capital providers to become more flexible to attract good operators.

Hopefully this framework can help you find the right search model.